your Fashion , food , lifestyle in one place

Many employees and HR professionals search for what is a lifestyle spending account when reviewing workplace benefits or comparing compensation packages. As employers look for flexible ways to support employee well-being, lifestyle spending accounts—often called LSAs—have become more common in benefits programs.

A lifestyle spending account is not a government-mandated benefit, nor is it standardized across companies. Instead, it is an employer-defined benefit that allows reimbursement for certain lifestyle-related expenses chosen by the employer. Because rules, eligible expenses, and tax treatment can vary, it is important to understand LSAs at a general, educational level before enrolling or using one.

This article provides a neutral, fact-based explanation designed to help readers understand how lifestyle spending accounts work, how they differ from other benefit accounts, and what limitations may apply.

A lifestyle spending account definition can be summarized as follows:

A lifestyle spending account (LSA) is an employer-funded benefit that reimburses employees for approved lifestyle, wellness, or personal development expenses, based on rules set by the employer.

Key characteristics include:

Funded solely by the employer

Designed to support well-being, flexibility, or work-life balance

Not regulated the same way as health savings accounts (HSAs) or flexible spending accounts (FSAs)

Unlike traditional benefit accounts, LSAs are highly customizable. Employers decide how much to contribute, what expenses are eligible, and how reimbursements are processed. This flexibility is one of the main reasons LSAs have gained attention in recent years.

Understanding how does a lifestyle spending account work requires looking at several basic components. While details differ by plan, most LSAs follow a similar structure.

Employers set a fixed allowance for employees

Funds are typically provided annually, quarterly, or monthly

Employees do not contribute their own money

Because LSAs are employer-funded, participation and funding levels depend entirely on company policy.

Employers define what expenses qualify for reimbursement. These categories may be broad or narrow, depending on organizational goals.

Most LSAs operate on a reimbursement model:

Employees pay for eligible expenses upfront

Receipts or proof of purchase are submitted

Approved expenses are reimbursed up to the available balance

Some employers use third-party benefits platforms to administer this process.

LSAs often include limitations, such as:

Annual spending caps

Specific eligibility rules

Deadlines for submitting claims

Unused funds may expire, depending on employer policy.

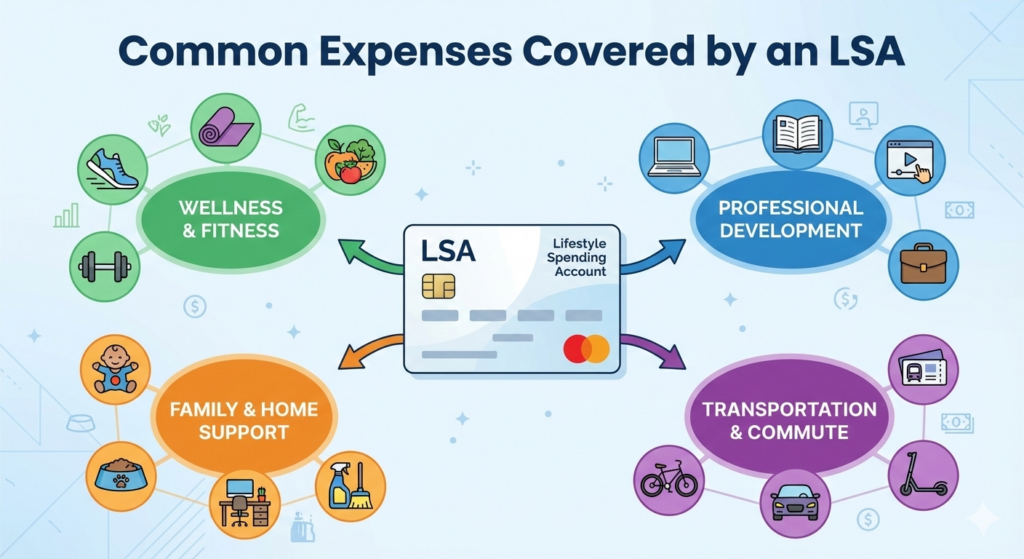

One of the most searched topics related to LSA benefits is what expenses are typically covered. While there is no universal list, common categories include the following.

Stress management programs

Mindfulness or meditation tools

General wellness services

Gym memberships

Fitness classes

Recreational sports fees

Professional development courses

Skill-building workshops

Educational subscriptions

Childcare support (in some plans)

Home office enhancements

Lifestyle services that support flexibility

It is important to emphasize that all eligible expenses are determined by the employer. What is covered under one employer lifestyle spending account may not be covered under another.

Employees often compare LSAs to more traditional benefits. Understanding these differences can help clarify when an LSA may be useful.

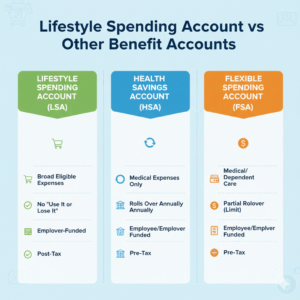

A common comparison is lifestyle spending account vs HSA.

Key differences include:

Regulation: HSAs are governed by IRS rules; LSAs are not

Eligibility: HSAs require enrollment in a high-deductible health plan; LSAs do not

Tax treatment: HSAs receive specific tax advantages; LSAs generally do not

The Internal Revenue Service (IRS) provides detailed guidance on HSAs, while LSAs fall outside those regulatory frameworks.

FSAs are also regulated accounts with defined rules.

Differences include:

FSAs have strict eligible expense lists

FSAs often have “use-it-or-lose-it” rules set by regulation

LSAs allow employers greater discretion

Wellness stipends are similar but often less structured.

Stipends may be paid as taxable income

LSAs usually require reimbursement documentation

LSAs are often administered through formal benefits platforms

Tax treatment is one of the most important considerations when learning about LSAs.

In general:

LSA reimbursements are often treated as taxable income to employees

Employers may deduct LSA expenses as a business expense

Tax treatment may vary by jurisdiction and expense category

The IRS does not classify LSAs the same way it does HSAs or FSAs. As a result, many LSA reimbursements are reported as wages on employee tax forms.

This article provides general educational information only and does not offer tax or financial advice. Employees should review employer plan documents and consult official IRS resources or qualified professionals for guidance specific to their situation.

Like any benefit, LSAs have advantages and limitations.

Potential benefits include:

Greater flexibility compared to traditional benefits

Support for holistic well-being

Access to services not covered by health insurance

Potential limitations include:

Taxable nature of reimbursements

Limited eligible expense lists

Funds may expire if unused

Understanding these trade-offs helps employees make informed decisions.

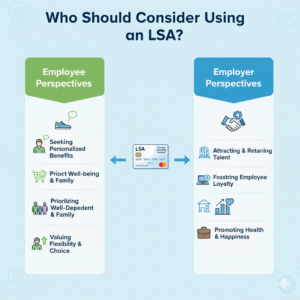

Employees who may benefit from an LSA include:

Those seeking flexibility in wellness spending

Individuals with interests outside traditional benefits

Employees who value personalized benefits

Participation is optional and should be evaluated based on individual needs and employer rules.

Employers may consider offering LSAs to:

Enhance benefits packages

Support employee satisfaction and retention

Provide customizable, modern benefits

LSAs allow employers to tailor benefits without changing core healthcare offerings.

In many cases, yes. LSA reimbursements are often treated as taxable income, though treatment can vary. Always review employer documentation and IRS guidance.

Some plans allow rollovers, while others do not. This depends entirely on employer policy.

No. Lifestyle spending accounts are optional benefits offered at the employer’s discretion.

Expenses outside employer-defined categories, cash withdrawals, and non-documented purchases are typically excluded.

Understanding what is a lifestyle spending account helps employees and employers navigate an increasingly flexible benefits landscape. LSAs are employer-funded, customizable benefits designed to support wellness, development, and work-life balance, but they are not standardized or regulated like HSAs or FSAs.

Because rules, eligible expenses, and tax treatment vary by employer and provider, it is essential to review official plan documents and ask questions before using an LSA. By approaching lifestyle spending accounts with clear expectations and accurate information, individuals can better evaluate whether this benefit aligns with their needs.

This general educational overview is intended to support informed decision-making and long-term understanding, not to replace professional or employer-specific guidance.

Kesha Smith is a lifestyle blogger passionate about simple living, healthy habits, and everyday inspiration. On this website, you’ll find